Beginner Budgeting with 50/30/20

Hi friends,

Making the decision to take ownership and control of your finances can seem daunting at first but it puts on us on the path to liberation. Liberation from confusion or shame relating to money. Liberation to a visible financial future we can see each month.

Last week, I spoke about the importance of an emergency fund and this provides a secure foundation for us to live our life. This week I want to talk about how simple creating a budget can be that acts as a guardrail for our financial decisions. This is via the 50/30/20 budget. I will talk about:

What the 50/30/20 budget is

Why it works for everyone in every situation

How to use the 50/30/20 budgeting rule

The positive impact of 50/30/20

What is the 50/30/20 budget?

As I’m sure you’ve worked out 50+30+20=100. The 50/30/20 budget aims to portion 100% of your take home income (that’s your pay after tax) into three simple separate categories: Needs, Wants, Saving/Paying off debt. These three categories are designed to track your expenses and identify where you can save more.

50% Needs. This includes things that you need in order to live your life. For example, your mortgage or rent, food, utilities, and transport

30% Wants. This includes things that you want but don’t really need to live. For example, holidays, clothes, eating out.

20% Savings. This includes any money you put away for the future whether that’s short or long term or towards paying off debt. For example, money in a savings account, investments in a Stock & Shares ISA, pension, or paying off credit card debt.

If you do have any debt it’s a good idea to dedicate all of the Savings portion towards paying it off as the interest rate on the debt will be higher than you can achieve in a savings account.

(If you’re repaying your Student Loan I wouldn’t count this like other debt but see it as more of a tax as it works completely differently to any other debt. So I’d disregard it from your 20% savings category!)

The rationale behind the 50/30/20 is it’s realistic and understandable. It allows your finances to be simply divided in three categories.

Why 50/30/20 works for everyone

The simplicity of the 50/30/20 budget means it’s applicable to everyone no matter how much you earn or how detailed you want your budget to be.

In its most simple form it can be used as a rule of thumb as the three separate categories are easy to create and offer a guide as to where you are spending your money.

It also allows more detail. It will let you drill down your expenses in detail assigning each one to each category to give you a complete split of where your money is going. And whatever approach you take is up to you!

The visual nature of 50/30/20 means you can easily see where changes are needed in your finances if your Wants spillover to 35% or if your Savings are falling below 20%. The guardrail nature of 50/30/20 makes it easy to identify where you need to get back on track.

How to use 50/30/20

Step 1 - Work out your monthly take home pay.

The best way to do this is by looking at your payslip which tells you what your pay is after deductions like tax. This step is necessary to start creating your 50/30/20 categories. If your pay varies month by month take an average over a year.

Step 2 - Work out your Needs.

Open your banking app or monthly statement, make a list of everything you spend in a month that is essential for you to live, and add them all up. For example, your food shop, rent/mortgage, council tax, gas, electricity, broadband, and insurances.

Step 3 - Work out your Wants.

A similar process to the Needs. Look through your monthly spending to identify things you pay for or buy that are nice-to-haves but aren’t essentials and add these up. For example, clothing, eating out, subscription services, TV packages.

Step 4 - Work our your Savings/Debt repayment.

Identify your current saving amount (including things like pension contributions) and any debt repayments. For example, putting money into a savings account or paying off a loan.

Step 5 - Is your budget in 50/30/20?

Once you’ve got the total of the Needs, Wants, and Savings you can work your current percentage split to each category. To do this you will need to divide each category by your take home pay total:

Needs Total ÷ Take home pay = Needs

Wants Total ÷ Take home pay = Wants

Savings Total ÷ Take home pay = Savings

This will give you the three percentages for each category so you can see how you fit in. If the percentages don’t align with 50/30/20 you can use the list you’ve just created to see what changes can be made to your outgoings.

Download this 50/30/20 budget template I have created to help you do this in more detail.

50/30/20 in practice

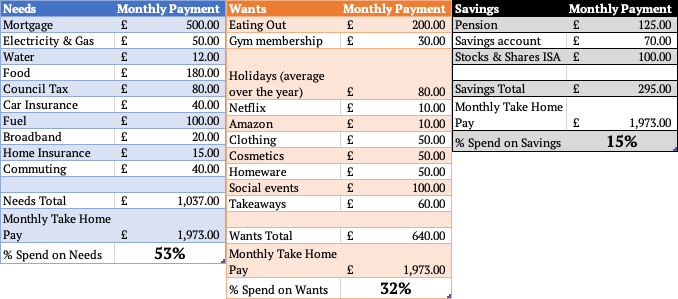

Sophie wants to take control of her finances through 50/30/20. She earns £30,000 a year before tax. Her take home pay each month is £1,973. She lives with her partner where they share costs for bills.

Needs - Sophie makes a list of the essentials bills or payments that she pays or contributes to every month.

Wants - Sophie make a list of all the nice-to-haves she pays each month.

Savings - Sophie adds together everything she saves each month.

As you can see, Sophie is overspending in the Needs and Wants category to give her a 53/32/15 budget.

To rectify this, Sophie could look at switching supermarkets to reduce her food costs or go on a comparison site for car and home insurance and broadband to find cheaper providers.

She could also look in the Wants category and consider reducing the amount she spends on eating out each month or on clothing and subscriptions.

Adjusting her spending to align with 50/30/20 would give Sophie an extra £100 a month.

This extra money saved could be added to her Stocks & Shares ISA. Over 10 years this could be the difference between £17,500 or £35,000 just by slightly changing her spending.

The positive impact of 50/30/20

Remember, 50/30/20 is just a guide. Once you’ve portioned out your spending into three categories it doesn’t need you mean to stick to the percentages rigidly.

For example, say you’ve worked out your Needs are only 45% and you’re actually Saving 25% every month. It doesn’t mean you need to change to a more expensive broadband provider, put the heating on in July, or switch from shopping at Tesco to Waitrose. If you’re saving 25% a month and you’re enjoying your life that’s great!

Moreover, if you’re paying off any form of debt it might be a good idea to switch the Wants and Savings percentages to 30% Savings and 20% Wants.

If you’re able to make this sacrifice temporarily and identify what Wants to cut out then the extra 10% on Savings can go towards paying off the debt. This means you’d be debt free quicker which saves you money in the long run!

Being meaningful in your 50/30/20 budget allows you to create financial goals for 1 year, 5 years, or ten years time.

Thanks for reading!

The template is great and super easy to use!